How to Avoid Upside-Down Car Loans

Published February 24, 2012 | Updated March 12, 2019

I'm sure you have heard thousands of car dealer radio ads that scream out "We'll pay off your car loan no matter how much you still owe!" This scam is aimed directly at people like you who might be under water on their car loans. Our consumer advocate team here at Carbuyingtips.com has been warning consumers about this new car advertising scam since we initially issued our Top 10 Car Dealer Scams way back in 1999.

Over the years our team of researchers and I have seen car buyers make many mistakes, and probably the worst financial mistake you can make as a car shopper is allowing yourself to become upside-down on your car loan. This is a battle that you lose before your even drive off the car dealer lot with your brand-new car. Your fate was sealed as soon as you decided you had to have that car no matter what.

When we say a car owner is under water on their car loan, being underwater means you owe more money on your vehicle than it your vehicle is worth at market value and based on feedback from our research of multitudes of car shoppers over the years, they usually end up between $5,000 and $7,000 underwater as most of our visitors tell us.

In fact, just last month we were helping a lady who was 6 months behind on her monthly car payments, so you can imagine how much under water she is being that late, and not paying off any principle all those months.

But how do so many people fall into this trap of being under water on their car loans? How could you possibly owe more money on your car than it is worth? We'll show you all about what it means to be upside-down on your car loan, how people fall into this upside-down trap, and how to avoid ever getting yourself into this devastating financial situation to begin with.

The Causes of Being Upside-Down on Your Car Loan

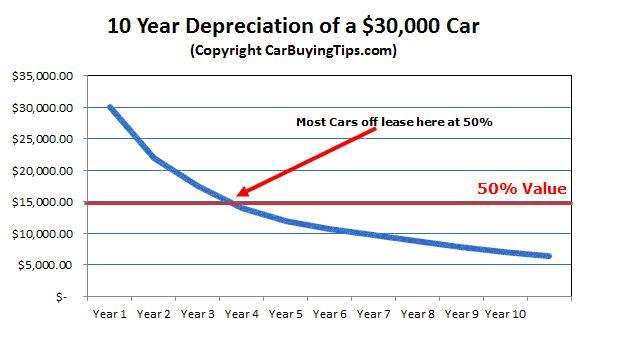

You must first understand how used car values work, in order to see how this upside-down car financing situation develops in the first place. The chart below shows a typical 10 year depreciation curve for most cars. The problem here is most people are unaware of this depreciation of value, and how it affects them and their car loan. They are blissfully unaware of their impending financial peril, that is until they are faced with a financial emergency and have to dump that car fast with a trade in.

This is when the car buyer is hit upside the head with a ton of bricks in the finance manager's office, when they learn the hard way that they owe more money on the car than it is worth. Don't let this happen to you, because now you are in a bind, and you either have to fork over about $5,000, or see if they finance the mount you owe into the new car. Congratulations, you are now paying off 2 cars without knowing it.

Unlike real estate, which for decades pretty much increased in value year over year, cars drop rapidly in value, and have their biggest drop in value in the first 3 years. The chart above shows a new car starting off with a $30,000 value, and losing about 25% of its value in the first year alone. By the second year, the same car has lost about 30-40% off its original value. By the 3rd year, most cars have lost about 50% of their value.

One talking point to mention here for you, is when you lease for 36 months, the leasing companies usually estimate the predicted final value of the car at the end of the 36 month lease, and they call this number the residual value, which is the market value of what they expect your car to be in 36 months. this residual value is usually about 50% to 55% of the original sales price.

This 3 year mark is shown above on the blue line when most cars come off lease for those who signed a 36 month contract, and the lease residual values assume there will be about 50% depreciation. The chart above shows us that the steepest part of the depreciation curve occurs in the first 3 years. If you trade in a used car, the dealer gives you thousands less than market value, further adding to your depreciation.

This is why we advise people to buy a 3-year-old used car instead, as the previous owner already took the depreciation hit. I bought a 3-year-old used Mercedes E350 for $27,591, and the original window sticker price was $62,300, a staggering 56% depreciation below MSRP in only 3 years. You can see even the pricey luxury brand names like Mercedes and Lexus all suffer depreciation too.

Also you will still have one year left on the manufacturer's warranty if you can buy a 3 year old car that has a 4 year manufacturer's warranty. You'll almost always get more money for your used car by selling yourself, but if you're upside-down and don't have the cash to pay the bank for the difference when you sell your car, then your only choice is trading it in, or refinancing your car loan to get your monthly car payments lower.

Adding fuel to the fire of being upside-down on your car loan

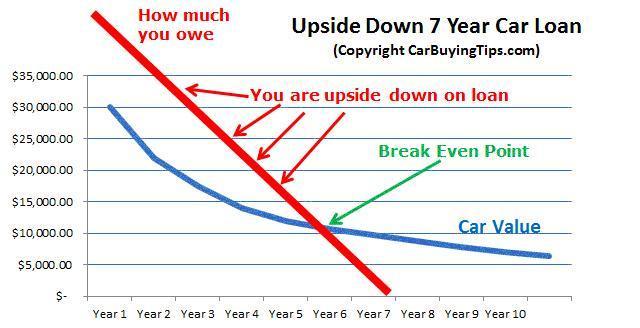

Knowing the above chart data we provided, you can look at the blue curve line and see that you should never take on an auto loan with a balance that is higher than that blue curve. The problem is many people put no money down after hearing the enticing car dealer ads, so right off the bat they owe more than their new car is worth. you just lost the financial battle the moment you heard that car dealer's ad on the radio.

Here is a great real-life example for you. Suppose you are buying a Toyota Highlander in the southeast with a selling price of $30,000 and 6% tax ($1800). Next the dealer sells you their add on extras and other useless nonsense like $400 VIN# etching, Dealer Prep of $600, Credit Life for $700, a $2,000 extended warranty, and the infamous $600 Toyoguard Protection Package.

Suddenly your $30,000 car purchase has ballooned up beyond control, to a staggering $35,500 purchase, significantly more than you thought you would be spending when you entered that new car dealership. Notice how all the extras add up to extra cost for you, but these overpriced extras don't necessarily add any intrinsic value to your car later on when you attempt to sell it.

Effect of high interest rates to people with less than perfect credit

Now assume you finance your new Toyota with no money down, so you are financing 100%. You borrow $35,500 for 72 months at 15% APR, you will owe a total of $54,046 by the end of the loan, because of the huge amount of total interest on your loan of $18,546! A person with a higher credit score than you might only pay 5% APR, with interest totaling a fraction of yours at $5,664.

What a staggering difference in suffering between you and your credit rich friend. This is where most people with bad credit don't see the unbelievable damage caused by financing a car with a high APR, just how badly it costs you. You are almost guaranteed to be upside-down on your car loan if you have a high APR, and the less you put down on your car loan, the more it will hurt you.

Don't make the mistake of just looking at the selling price of the car, because that is not the amount you owe. With extras and interest, your actual amount owed can be $5,000 to $20,000 more than the car itself. This is what trips everyone up so badly, because never in your wildest dreams would you consider that you owe many thousands more than the price of the car.

What makes things worse for you is that most of the interest is paid in the front end of the loan, so your principal is getting paid off at a much slower rate than the interest. The resulting scenario is if you buy the car today and you need to sell it quick one year from now, it will only be worth about $22,100 but your loan payoff will be much more than the value of the car, usually at least by $5,000 according to most of our visitors who contact us.

Now you're stuck big time, and you're at the mercy of greedy salespeople who take advantage of your situation to low ball your trade in, using their cash flow shell games to confuse you, blind you, then rob you of the value of your trade in. This is why you hear these commercials, because it's a feeding frenzy, and you're the feast, they prey on thousands of financially uninformed consumers just like you.

Disturbing trend: Car loan periods stretching out 72-84 months

Adding more fuel to this fire is a news report from CNBC some years back reporting 6 year and 7-year car loans were up by 47%, which we here at CarBuyingTips.com find to be very alarming. This means more and more people are violating our financial wisdom rule of thumb where we tell you to avoid financing a car longer than 48 months.

It also means Americans are putting aside their common sense and not managing their money properly. Do you really want to be paying off a car for 7 years? It's becoming the norm, so now everyone is being corralled by the car dealers into long term loans so they can sell more cars at the expense of putting you in a poorly leveraged financial situation.

These car salespeople are training you just like feeding the ducks into accepting this as the new norm. If you stretch out the loan to 6 and 7 years, you will fall much farther behind the depreciation curve, and be even further upside-down. It will take you too long to reach the break-even point where the car is worth more than you owe.

Sadly, we've seen too many car shoppers who never reach the break-even point, because they are trading in their car which they owe money on, they take out loans that are too long, and their bad credit has them in a high APR car loan. It's the perfect trinity of financial disaster, and they keep dipping themselves out of one car loan and into another loan accumulating more debt as time goes by.

The reason people are choosing longer car loans is because they want the lower monthly payments, and they refuse to settle for less car. The younger self entitlement generation wants the best no matter the cost, and they stand there with their hand out for help when it fails them.

You should always analyze whether you should be buying that car now, or if you should wait until you have 20% of the value of the car to put down. Now with increased extended loan terms car shoppers become slaves to their car payments and mortgages, which consume their lives. This chart below shows you visually how car buyers get upside down on their auto loan, by simply borrowing more than the value of the car, so the red payoff line there is steeply above the car's value until the break-even point usually until year 5 or 6.

In the chart example below, you could improve things a bit, by doing a 36 month loan, you can imagine how the red line would change, ending at Year 3 instead of Year 7, but you can see that you would barely break even by time you pay off the loan in 3 years.

Major factors causing you to be under water on your new car loan:

- Natural depreciation curve of car values

- Car dealer low balls your trade in value

- Overpriced dealer add on items like VIN etching, high priced warranty, credit life insurance

- Putting down less than 20% on the car

- Car loans longer than 48 months

- Damage or excessive wear and mileage on your car

- Market conditions like gas prices at $4.50 and no one wants to buy your used SUV

Car dealers take advantage of you in your upside-down car loan situation.

All those unethical car dealer radio ads are designed to draw you into their lair where they pull out the stops and unleash all their tricks on you. People who are upside-down on their loans are the biggest victims providing dealers with some huge profits, this is why you hear these ads all over the place, there is a lot of money to squeeze out of undisciplined foolish people who spend with their hearts and not their brains.

These transactions are a very complex set of smoke and mirrors which is why they rake you over the coals so easily, like stealing candy from a baby. Here's what the dealer is really doing to you by "paying off your loan no matter how much you owe:"

- They sell you a new car at full price because you're desperate to get out of your car

- They low ball your trade-in even more because you're desperate and don't understand the numbers

- The car dealer pays off your current car loan with your current lender

- Next the car dealer rolls that payoff amount into your new car loan

- Now you are paying off 1½ cars instead of 1 car before

Hey, how many of you were speed reading so fast that you missed the 1 1/2 cars statement above? Most people have no idea they are now paying off effectively 2 cars after completing this transaction. That's right folks, this is the core of their scam, you are still paying off what you still owed on the first car, plus you are now also paying off your new car!

The beauty of this scam is most victims don't even know they are a victim. The finance manager spreads out the monthly payments over 7 years which sometimes causes you to have a lower payment and still think you're saving money. But in fact you're lining the dealer's pockets with thousands more over those 7 years.

What started out originally as maybe your 5-year loan elsewhere a year ago, just got renewed to a 7 year loan, meaning you are now looking at additional years to pay off your car, plus the dealer managed to sell you a new car at the same time! We can assure you that you had no business buying that new car either, just like you had no business being in the original deal that you had.

The car dealer dipped you out of your current loan, and dipped you into their new loan, now you owe all that money to them. They are laughing and high-fiving as you drive off with your new car, oblivious to the danger you just put yourself in. Years after you drive out of the dealership, you'll still be paying the price for your ignorance, so we are here to help you avoid this scenario.

One of the worst mistakes consumers make when trading in a car

Most car buyers think that trading in their current car means they no longer have the burden of that debt any more. This is what gets all the victims.

Do you see what the dealer just did to you above? They tricked your brain into thinking they paid off your loan and you falsely think that you are no longer a slave to it. Listen to our warning here that one of the worst mistakes consumers make when trading in a car is they think that trading in a car means they don't have that debt any more.

This is just what unscrupulous dealers want you to think. If you owe $10,000 on a car when you trade it in, you still owe that debt to someone, it does not just disappear. It might not be your original lender that you owe the $10,000 to anymore, but you do still owe that $10,000 debt, it does not just disappear.

This is where consumers get it so wrong, failing to understand the mechanics of owing a debt. Think of a debt as excess luggage that follows you everywhere you go.

How to prevent being upside-down on your car loan

Now that you know the mechanics of what causes this scenario, it's easy to avoid it. The basic strategy is to always be sure you are borrowing much less than the car is worth. We have been advising consumers on this since our inception over 20 years ago. We have always suggested putting down 20% on the car and finance no longer than 48 months. That is how you prevent upside-down car loans.

If you cannot put down 20% or handle a 48-month car loan, then do not buy the car, it's that simple. Do some soul searching, learn to live with less, but make sure you remain inside our time tested CarBuyingtips.com guidelines that we outline for you here below; our guidelines are designed to keep you out of trouble.

If your pride is unwilling to settle for something that fits your budget, and you think we're just on our high horses dispensing meaningless wisdom, and if you want to get into trouble, then by all means ignore our advice.

We are on a mission to get all of us and you and your friends and family all living within our means. We are telling you that 48 months is the limit of our means. If we can't get a sustainable monthly payment to fit into these limits, then we are not living within our means, and we need to correct it now, or we'll veer of course later.Our summary of car buying tips to avoid being upside-down on your car loan

- Put down 20%, make sure your car loan amount is lower than the selling price

- 48-month maximum car loan term. 36 months is even better

- Avoid the overpriced extras at the dealer

- Don't attempt car financing until you have checked your credit, confirmed it's clean

- Try to get the lowest APR loan possible

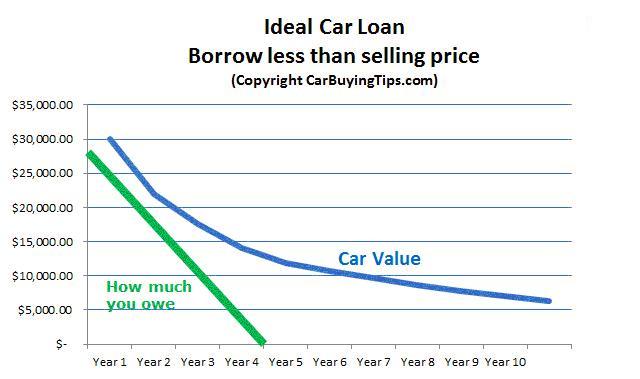

The chart below shows how your car loan should be structured. Using our same Toyota example earlier, the $35,500 total purchase should have a down payment of 20%, or about $7,000.

This means in the above example we should not borrow more than about $28,000, which is comfortably less than the new car value. See how our green line stays below the car value depreciation curve the entire time. Try to pay off your loan as soon as possible sending in extra principle whenever you can; you will save a lot on interest too.

We prefer to pay our car loans off in 3 years, but the Mercedes I bought for myself I was able to pay cash, and I also paid cash for my daughter's first car, which was $9200. If you're stuck in a high APR loan right now, look into refinancing to a lower rate to reduce your payments.

You should never trade in your car to buy another car in an attempt to lower your monthly payments. Be sure to think everything through before you buy, and keep all our advice in mind, and you'll enjoy financial peace in your life.

About The Author: Jeff Ostroff

A lifelong consumer advocate with over 20 years of unparalleled expertise, Jeff is the Founder, CEO and Editor-In-Chief of CarBuyingTips.com. As chief consumer advocate, he oversees a team of experts who cover all aspects of buying and selling new and used cars including leasing and financing.

For decades, Jeff has been the recognized authority on vehicle purchasing, sought out often by the media for his decades of experience and commentary, for live call-in business radio talk shows and is cited often by the press for his expertise in savvy car shopping methods and preventing consumer scams and online fraud. Jeff has been quoted in: CNN, MSNBC, Forbes, New York Times, Consumer Reports, Wall Street Journal and many more.

Jeff also has extensive experience and expertise in new car brokering and selling used cars for clients on eBay and Craigslist. Connect with Jeff via Email or on Twitter.