How to Buy a Used Car with a Loan Balance

Published June 27, 2012 | Updated March 15, 2019

Many car shoppers find themselves perplexed by the intricacies of car financing and ask us here on CarBuyingTips.com, "How do you buy a used car from a seller who still owes money to the bank for the car loan, and how do you transfer the title to your name?" You just agreed to buy a used Honda Accord from a seller on eBay Motors or Craigslist for $10,000 then you learn the seller still owes $3,000 on the car loan. What do you do now?

Our consumer advocate team wants to make sure you are as protected as a savvy consumer can be, so be sure to read our full used car buyer's guide Buying a Used Car - Tips and Scams to Avoid. Do not venture out to buy a used car until you have read all sections of that used car buyer's guide.

The used car buyer's guide also has our printable list of Questions to Ask a Seller When Buying a Used Car. Print that list out and bring it to the seller as you inspect cars, and ask the seller these grilling questions.

Who really has the title to the Honda Accord and how do you get the title and get it into your name and be sure the loan gets paid off? Here are all the critical logistical details you need to consider to bring this used car sale to fruition.

If you are researching a used car extended warranty, read our buying guide first

since you are buying a used car and you might be researching used car extended warranties, read our consumer guide on how to buy extended warranties and avoid scams. Read the complete Extended Warranty article. It gives you an easy to follow education on the inner workings of used car extended warranties, and all the contract coverage pitfalls to avoid.

Do not buy an extended warranty for your used car until you read that guide, or you will not be properly prepared to make any sane purchase decisions.

This type of transaction seems puzzling and complex to people, but it's really quite simple, with 2 minor hurdles to overcome:

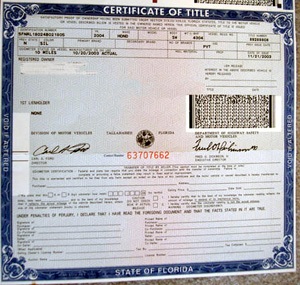

Hurdle #1: The Bank Holds Your Title When You Finance a Car

When you buy a new car and finance it, you legally own your car, your name is on the title and registration, but maybe this slipped your mind: the bank is holding the title in their possession! Remember, you don't have the title. This means you cannot sell the car to another person until you satisfy the car loan in full. If you fail to do this, the lender will still hold the title, and you cannot legally transfer the title to a buyer without having the title to sign it over.

The lender is listed on the front of the title as a lien holder. They hold the title so you can't sell the car until you pay off your car loan. Vehicle titles are electronic when held by the bank and must be printed once the loan is paid off. Then the lender/lienholder sends you the title, now you can legally transfer ownership of your used car to the buyer.

Hurdle #2: The Bank Delivers the Title to the Current Owner Only

The second slight hurdle to overcome is the lender has a business relationship with the person who is selling you the car. That person is the bank's customer. The bank will never send you, the buyer of that car, the title directly. Even if you provide the check to the lender to pay off the car, the lender still won't send the title to you, only the borrower, because you are not the borrower in this loan.

Once the loan on the used car is paid off and the bank is then satisfied, about a week later they send the clear title to their customer free of liens, with "Lien Satisfied" stamped on the front of the title. Now the seller legally owns their car without encumbrances.

There might still be cases where the lender is still listed as lienholder, but if you have the title in your hand, It's because the title is clear of liens, you can confirm with the lender, but it should be clear.

Our consumer advocate team has successfully negotiated these waters when helping used car sellers list their used cars for sale online with an outstanding loan balance. We have developed these outline steps below and they stood the test of time. Before you pay off a car loan with a lump sum payment, you need to call the lender and obtain a "payoff figure" from them which is good usually for 10 days.

If you fail to pay off the loan after 10 days, the interest resumes accruing, and you'll have to start the process all over again with another phone call, and a new payoff figure, or you'll have to pay more as the interest is accruing.

How to Keep the Seller Accountable When you Pay

When you buy that used car, you would be justifiably nervous about giving the seller all this money and wondering "what if she does not pay off the bank?" This is why you must keep sellers accountable and make payment directly to the bank, not the seller. Make sure that lender is paid in full, only then are you assured that the lien is at least satisfied.

It's too risky to give all the money to the seller. What if they get robbed, scammed, have a medical emergency, or they could be a drug addict, or otherwise misappropriate the funds and never make it to the bank to pay off the car loan? It's like helping out poor people, you never give them cash, you instead buy them food or pay an electric bill on their behalf, and it's all about accountability.

When paying the bank off, if there are funds left after satisfying the loan, you can pay leftover amounts to the seller. The seller could theoretically still scam you and not deliver the car, but at least he did not get your cash directly.

If the lender is not paid off, you will never get the title...Ever

If the lender is not satisfied, you'll never get the title to the car no matter what. The lender does not care if you bought the car and paid money to the seller, the lender never got their money, and they hold the purse strings, the title strings, and your sanity strings.

Be sure to download our free Used Car Bill Of Sale Spreadsheet from our free download section, to use as your invoice, and for DMV supporting paperwork.

How you get the used car title once the car loan is paid off

Once the bank is paid off they send a clean title to the seller of the car. The seller is now obligated to deliver that title to you in person if you are local, or by FedEx. I only recommend FedEx, not the postal service, get a tracking number and follow the progress of the FedEx delivery online. A best case scenario is to ask if the seller can accompany you down to the DMV office in case any questions arise during the title transfer.

Use second-day delivery to save money. Once you receive possession of the official title from the seller, visit the DMV office in person and have the title transferred into your name.

Summary of steps to take to ensure a smooth used car title transfer

Here's a summary of our steps for you to take when buying a used car with an outstanding loan balance:

- If the seller still owes money to a lender/lienholder, get a certified check payable to the lender

- Any leftover funds after paying off the lender go to the seller

- Use our bill of sale form mentioned above signed by you and the seller

- Send payment to lender with loan account number on it to pay off the car loan

- After a week the lender sends the title to the seller (not to you)

- Seller signs title over to you, delivers to you

- Bring title and bill of sale to DMV, transfer title to your name, life is good

This should be smooth sailing for you. Good luck out there!

About The Author: Jeff Ostroff

A lifelong consumer advocate with over 20 years of unparalleled expertise, Jeff is the Founder, CEO and Editor-In-Chief of CarBuyingTips.com. As chief consumer advocate, he oversees a team of experts who cover all aspects of buying and selling new and used cars including leasing and financing.

For decades, Jeff has been the recognized authority on vehicle purchasing, sought out often by the media for his decades of experience and commentary, for live call-in business radio talk shows and is cited often by the press for his expertise in savvy car shopping methods and preventing consumer scams and online fraud. Jeff has been quoted in: CNN, MSNBC, Forbes, New York Times, Consumer Reports, Wall Street Journal and many more.

Jeff also has extensive experience and expertise in new car brokering and selling used cars for clients on eBay and Craigslist. Connect with Jeff via Email or on Twitter.