Shockingly Misleading Car Lease Advertising

You see advertising all the time for car leases at very low monthly payments. They entice you with the dream of driving a great new car for a very affordable monthly payment. Who wouldn't want to take advantage of this kind of deal?

Of course you know deep inside that car manufacturers and dealers aren't in the business to give you great deals. They just want you to THINK you are getting a great deal. Their marketing tactics rear their ugly head in ads for leases more than anywhere else. We are going to go through some examples to show you what kind of sleight of hand you must be prepared to deal with.

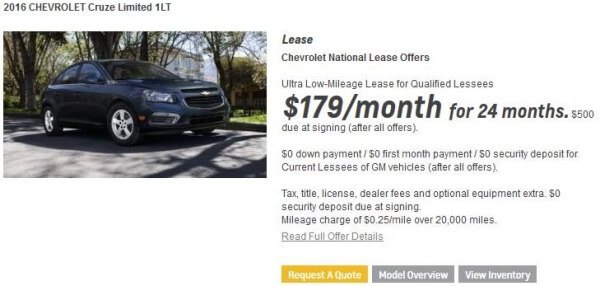

So that you can see an example, let's take a look at an ad for a Chevrolet Cruze lease. We aren't just picking on Chevy or General Motors, you'll see similar ads from all brands but we needed to select one to point out the key details.

Lots of Fine Print

As with a lot of advertising, car leasing ads contain a lot of fine print. This fine print can change what is apparently a really good deal into a bad deal very quickly. The caveats will apply to the majority, if not all, of the customers.

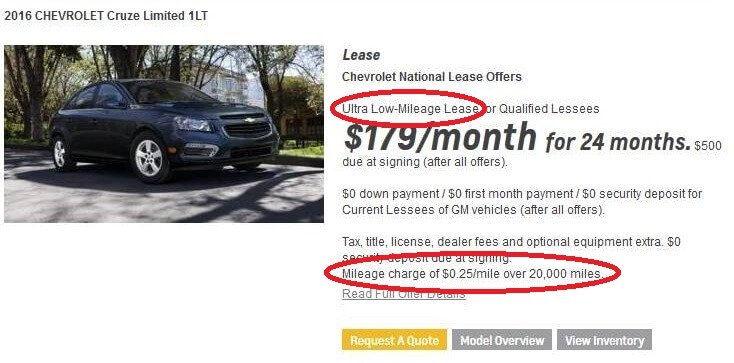

Beware of Ultra Low-Mileage Leases

One of the most egregious examples of deceptive advertising that we have found are ads that are for "Ultra Low-Mileage Leases." Some people may be able to take advantage of these offers but they only work if you don't drive very much.

Notice that this lease only gives you 20,000 miles over the two year term (10,000 miles per year). According to the U.S. Department of Transportation Federal Highway Administration (since we like government acronyms let's call it the USDOTFHA), the average driver drives 13,476 miles per year. This means that, on average, people will use 3,476 miles per year more than is allowed by this lease deal. At $0.25 per mile for the overage charge, this works out to an average penalty of $72.46 per month.

It is time to slam on the breaks and dig into that penalty! The lease deal is being advertised for $179 per month. The $72.46 per month that an average driver will be charged in penalties will increase the monthly cost by a whopping 40%. Your $179 a month lease has just turned into a $251 per month lease just by being an average driver! How does this great deal look now?

Of course, not everybody drives the average mileage. Even the averages vary by age and gender. To see the breakdown, click here for the date on the USDOT website.

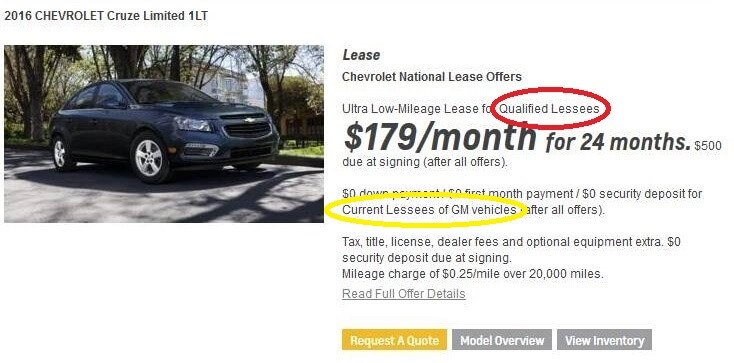

"Qualified Lessees"

Lease ads will usually have some statement in the fine print that make it clear that the deal is only available to "qualified lessees." Until you sit down with the finance manager, you won't know if you are among the lucky people that are qualified for the deal. The qualification is normally based on your credit rating, since leasing is really a type of finance product.

With a lease, you are basically financing the depreciation instead of financing the purchase price. Still, putting the qualified lessee caveat in the fine print gives them a lot of wiggle room to rake you over the coals. They can lie about your credit score and tell you that you have to pay more per month because of it.

Current Manufacturer Lessees

An additional note about who is qualified for a deal. In our example, you can see that this deal is only for "current lessees of GM vehicles." Even if you own a GM car or truck, you don't qualify for this deal. Instead, you will be drawn into the dealership under false pretenses and they will try to get you into a deal that is more beneficial to them.

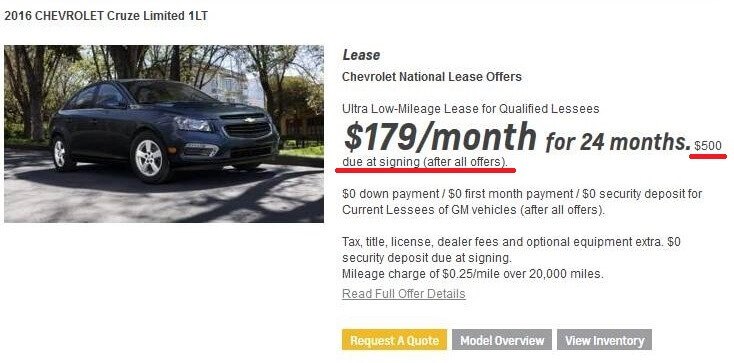

The "Due at Lease Signing" Trap

When you buy a car outright, you expect to make a down payment. That is OK because you are putting equity into the car and reducing the interest you end up paying on the loan. When you are leasing, you are essentially renting the car for a long term period of time. Making a down payment doesn't give you any benefit because you won't be able to sell the car and recoup equity at the end of the lease.

The amount due at lease signing is similar to a down payment. It is used to lower the monthly payments. On the surface it doesn't seem like there is any difference from a purchase. You are paying money up front to pay less on a monthly basis. However, in this case, your down payment is being used to create the deal. The only reason you can pay $179 a month is because you are putting down $500.

They are using your money to give you a deal. That would be like going to the grocery store and them telling you that something is 50% off but you have to pay a 50% down payment first. The $500 due on this particular deal isn't that much, but many deals can have another zero added to the end. That will change everything.

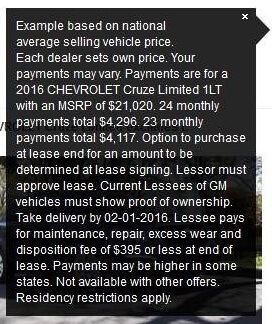

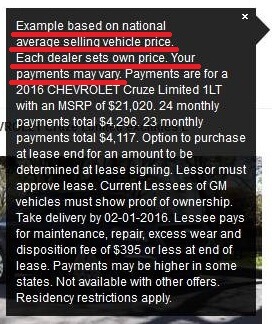

When is the Price not the Price?

Apparently, when you advertise a lease deal, the monthly payment doesn't even have to be offered. Look carefully at the fine print in this screen shot.

It says, "Example based on national average selling vehicle price. Each dealer sets own price. Your payments may vary." WHAT? So basically they are saying that the payment is based on an average price and that each dealer can charge whatever they want. That doesn't seem like very straightforward advertising to me. A dealer could decide to charge $200 more and require $700 at signing instead of $500 to get the same monthly payment.

Go to a Reputable Dealership

The best way to get the deal you think you are getting is to find a reputable dealership. We recommend shopping multiple dealerships. By negotiating with several dealerships, you can easily weed out the ones that are trying to pull one over on you.

Begin by getting a guaranteed price certificate from TrueCar. This will at least eliminate the issue of the dealer inventing the cost. They can still play around with things like the money factor or lease term so don't let your guard down.

Once you have the certificate in hand, get additional quotes from RydeShopper and Edmunds.

Before you head out to sign the papers, you should read our complete car leasing guide so you understand the entire process.

About The Author: Lyle Romer is a consumer advocate, Founding Contributor and Vice President of CarBuyingTips.com. A 20 years veteran of the auto industry with a high level of expertise, Lyle has been researching all aspects of the automotive sales industry.

Lyle's expertise and research played a vital role during the creation of CarBuyingTips.com in 1999 after years of industry research. He carefully observed every aspect of his own car buying experience as the internet began to take a foothold in the process. He also designed the site to make sure that consumers had easy access to the best consumer advocate education.

Lyle has been an auto industry insider since 1999. He also has worked with other automotive websites to help improve their offerings based upon feedback from CarBuyingTips.com users. He covers important industry events and gathers off the record sources while attending industry conventions.

Connect with the author via: Email