How to Create Your Own Extended Warranty

When you can't get coverage for your car

Many people want to buy an extended warranty when they buy a new or used car. But sometimes they are disappointed to learn that the warranty company refuses to cover their particular car. They try other companies only to face the same rejection. I hear it all the time from our visitors buying old high mileage cars or even some new car brands; they can't find a company willing to cover them. What would you do? What advice do we give them?

Just a quick technical point first, according to U.S. law, warranties can only be offered by the manufacturer, so the industry really calls them Vehicle Service Contracts (VSC) or agreements. But that's way too much of a mouthful to me, and I'm lazy so I'll use the terms interchangeably here.

Last week one of our CarBuyingTips.com visitors named Steve who is shopping for a 1969 Ford Mustang asked me "Jeff, where I am going to locate an extended warranty company that covers classic cars and if there are any, are there companies that offer exclusionary and wear and tear coverage?" We must realize that buying high mileage, very old or classic cars presents a problem.

I have years of experience dealing with this very issue. We all want to get the best coverage and we want icing on our cake. I can imagine the folks at the company laughing as they look at the request for quotes of some cars that are just not coverable.

Since I've been in the automotive world for so long, I personally interact with the top management of several warranty companies. I have good insight into what they go through as well as the thousands of car buyers who visit us every month to be educated. Before we can answer the question of why they won't cover certain cars and how can we then get coverage, let's quickly look at how the industry works.

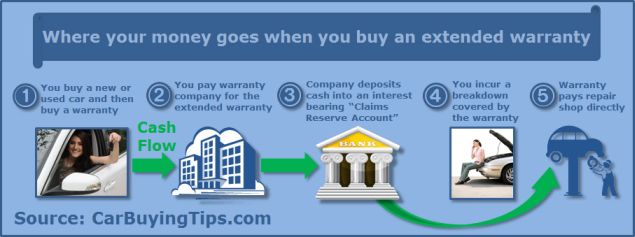

How warranty companies make money and where the funds go

In a simplified explanation, when you buy your Vehicle Service Contract from the company, their actuaries have already applied all the known historical repair data on your car to determine how much to charge. That's why you have to enter all the make, model, year and mileage before you can get online quotes. The company then takes the money you pay them and deposits it into an insured Claims Reserve Account, a type of investment account that bears interest.

They hope you never make a claim so they can keep 100% of the money you paid them. If you have a covered claim, they hope it's small, and that the interest earned on the account will help cover their costs. They usually pay the repair shop directly, to a lower negotiated rate than you and I could get it for.

Why the companies won't cover your car

Now that we know how the companies deal with the money and pay the repair claims, you can see how they try to avoid unnecessary risk. Similar to insurance companies, who will cancel your home owner's insurance if they find out about that large trampoline in your back yard, vehicle service contract companies won't cover vehicles which are going to be too expensive to repair or which have a high rate of failures.

If you live in California, that is a special case because there are very few companies who are legally allowed to sell warranties online there. They must be registered as licensed insurance agents in order to sell in California and many don't want to bother with it.

Cars which are typically rejected by warranty companies:

- Cars over 10 years old

- Vehicles that have over 100,000 miles

- Vehicles titled in California

- Land Rovers

- Mercedes AMG

- Exotic brands such as Ferrari, Lamborghini, Bentley, etc.

- Vehicles with a super charger

- Models with historically high repair costs or failure rates

This is not an all-inclusive list, but it is the norm for most companies you will come in contact with. Keep in mind that even if you do find a company to cover your car, you are likely to discover they won't sell you their most premium plans with the most coverage for wear and tear. Often you will be sold a diluted down named component coverage that covers a smaller list of components on your car. Some might only be willing to sell you a powertrain warranty that only covers some of the engine and transmission basics, but no wear and tear. It often ends up not being worth your money.

How to create your own extended warranty

Well now that we know we might be sitting with a car that we can't get a service contract for, what can we do about it? Wait a minute, I have a brilliant idea. Here's what we do. We use the same strategy that we've been telling our CarBuyingTips.com visitors for years. Let's do the same thing the companies do.

Remember above we showed how the companies manage the money and make the payments to the auto repair shops? Let's copy them and do what the pros do by setting up our own Claims Reserve Account. This is just my fancy name for a rainy day savings account. Just take $2,000 or more and deposit it into your account. If your car is expensive to repair and has a history of breakdowns, you should put more money into your account. You can also split the funds up into a few certificates of deposit, which you can redeem whenever you have a needed repair.

Your claims reserve account can also be put into slightly more aggressive mutual funds or ETFs. Be aware though, there is risk that investment accounts can drop in value during challenging market times. We know we'll have recessions every 6 years or so, but stocks have historically always recovered. Our strategy is explained clearly in this infographic below:

The real beauty of our strategy here is that you'll never reject any of your own repair claims. Also if you have not made any claims against your account to pay for any repairs, then you'll have a few grand extra lining your pockets, just like the service contract companies would have. This is just like finding money in your laundry. Let us know how you did with our advice and like always, contact us with any questions.

About The Author: Jeff Ostroff

A lifelong consumer advocate with over 20 years of unparalleled expertise, Jeff is the Founder, CEO and Editor-In-Chief of CarBuyingTips.com. As chief consumer advocate, he oversees a team of experts who cover all aspects of buying and selling new and used cars including leasing and financing.

For decades, Jeff has been the recognized authority on vehicle purchasing, sought out often by the media for his decades of experience and commentary, for live call-in business radio talk shows and is cited often by the press for his expertise in savvy car shopping methods and preventing consumer scams and online fraud. Jeff has been quoted in: CNN, MSNBC, Forbes, New York Times, Consumer Reports, Wall Street Journal and many more.

Jeff also has extensive experience and expertise in new car brokering and selling used cars for clients on eBay and Craigslist. Connect with Jeff via Email or on Twitter.