9 Strategies You Control to Lower Your Car Loan APR

Tips for stretching your dollar and reducing your interest paid over the life of a new car loan

Too many car buyers pay too high of an interest rate on their car loan. Either their credit history is dotted with poor financial management land mines, or car dealers lie to them, railroading them into outrageously high APR. Sometimes people are simply unaware of certain strategies that they were in control of which can lower their APR.

We have compiled this list of proven strategies that we have advised consumers to use over the years. You don't have to take whatever financing a car dealer is shoving down your throat. There are many processes here which you may have never thought of, that are under your control which you can easily use to save the most money possible.

We'll show you all the tricks to lower your APR on your new car financing, as well as how to refinance an existing high APR car loan to a lower rate. Here are your 9 APR lowering strategies:

1) Be patient and don't rush into a car loan

One thing is for sure, us humans are instant gratification entitlement freaks. We see that car we want and we head right out to the dealer to buy it. We don't even considering the car finance aspects of this new acquisition. We expect that we're going to be approved for a loan at 0 to 2%. Next thing you know you're paying 11% for 72 months, because fools rush in.

The savvy car buyer is patient and willing to wait and carefully plans their entire car finance process, which can take 6 months of planning and execution. Are you patient enough for this? If so the rewards can be big. Many people have errors in their credit file and we all have a credit score that needs to be improved before we should ever consider applying for an auto loan. These strategies can take a few months to clear up and have them reflect in your credit score.

One other thought to keep in mind when you see lenders advertising their low APR interest rates. Those numbers are for "well qualified buyers." Unless you have a 700 or higher credit score, you'll pay higher interest than the commercials dangle in front of you.

2) Pay off your credit card balances to get a lower APR

Potential lenders hate to see you with high credit card balances. It does not give them a warm and fuzzy feeling about your ability to make your monthly car loan payments when you are saddled with 21% APR credit card interest payments. The higher your debt load, the potentially lower your credit score can be, so reducing your debt below the 30% credit limit mark will help increase your score, which leads to lower interest rates.

For some of you this will make the difference between getting approved and not getting approved, regardless of the interest rate.

The closer you can get your credit card balances to zero, the better. Then wait a month or two for the credit bureaus to update to your new lower account balances to positively affect your credit score before applying for a car loan.

3) Sell under-performing stocks to buy down your credit card debt

Here's a great idea I came up with years ago that probably no one ever considers it, but it's ripe for the plucking for many people. All of us at one time or another have owned a stock that is performing so poorly it has become a "dog with fleas" as Gordon Gekko calls it in Wall Street, one of my favorite movies.

I have had a few stocks over the years that just sat in my investment accounts doing nothing but tying up a few thousand dollars and this really stinks, because it is also lost potential earnings, or savings on a lower interest rate. But, you can take this dog with fleas and turn it into man's best friend for you by selling that lousy stock and officially "realizing that loss." Now you have the proceeds from selling that junk stock to work with in a positive manner to reduce your credit card debt or add to your down payment and this will help you out in the long run.

You also will have a tax loss that can be used to reduce your tax liability for the year, reducing you adjusted gross income and possibly giving you a larger tax refund to spend on a new car.

For decades we here at CarBuyingTips.com have been pounding the tables telling people not to pay credit card interest of 18% to 29% because you'll never get out of it. Since higher credit card balances drag down your credit score and if you are still clinging to a lousy stock, let this old dog with fleas of rescue you from higher interest rates by paying off as much of your highest APR debt with the proceeds of selling this stock.

Honestly, if you have any credit card debt that you are paying interest on, you should sell any stock you hold (except in retirement accounts) to pay it down. Most stock holdings will not earn enough yearly to earn more than the interest rate you are being charged by a credit card.

For some of you, this could bump up your credit score enough to make all the difference in the world. You can go from getting rejected to getting approved for your car loan. Paying down your debt is all under your control and is one of the most powerful tricks in the car shopper's arsenal of weapons in the war on saving money.

4) Get car financing online instantly instead of through a car dealer

Over the years the savviest visitors to our site wait until their credit score improves, then they obtain pre-approval instantly from online auto loan sites such as LightStream.

What is the benefit to you and I from applying for car financing online? You get your financing ducks in a row before ever stepping foot into the car dealer. We bypass the car dealer and get much better interest rates online.

Unless you are approved for one of those rare 0% loans subsidized by the car manufacturer, you could be paying high APR interest rates through the car dealer's financing.

Quite often the efficient online car finance sites with lower overhead beat the rates of the car dealers and some lenders deposit the loan money right into your bank account to use for buying your new car.

Compare that to applying for your car financing at the dealer, where they will sometimes call a week later to tell you the deal fell through because their lender rejected you.

This nonsense never happens with online lenders. You are in control here, not the car dealer. You get your answer a yes or no right away and no games. Once approved, you car loan money is in your account quickly or a check is sent via overnight delivery.

5) Refinance your existing car loan to a lower rate

This is a very powerful way that you can chart your own destiny to save a lot of money if you have any existing high APR car loans. Many people get lost in the here and now shopping for a new car, forgetting they are already a prisoner already to a previous high APR auto loan. So remember that buying a new car is not just about this new car, but rather it involves your entire financial picture.

Does your current financial picture involve you having an existing car loan with a high APR? Maybe a car dealer scammed you on a previous deal with a super high car loan interest rate? This happens all the time.

Perhaps you previously had questionable credit scores and were railroaded into high APR auto financing with little time to think it over. Now you are on the mend, but you still have that high APR baggage from your previous life. You could refinance to a lower APR by using online lenders such as LightStream and CARCHEX.

This is a useful strategy for you to use. Not only are you saving money on your new car using all our consumer advocate advice here and also potentially getting a lower new car loan APR. You are also saving more money on your existing loans by stopping your higher interest rate in its tracks. The money you save by refinancing your previous car loan to lower rates can help pay for your new car.

6) Choose lower car loan terms with fewer months

This strategy is another parameter under your control and is equally as effective on new car loans as it is on refinancing. This is one of those great moments in life where less is not more; less is less. Are you one of those people who focus on cramming as much car into a 72 month payment as possible? If this is true your ideology needs to change right away. Our top advice over the last 15 years has always been to pay off the loan in as few months as possible, never more than 48 months.

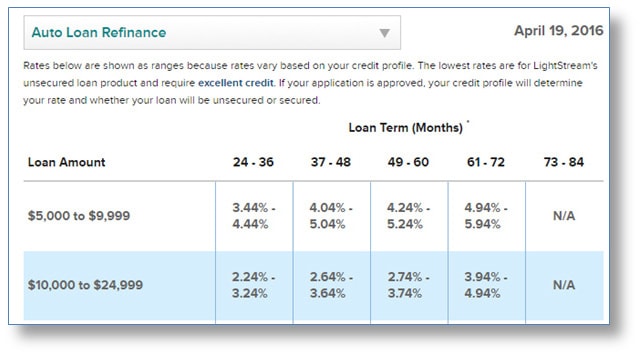

Look at this snippet below from Suntrust Bank's LightStream web site which was current as of the time of this writing. Most of us will be looking to refinance at least $10,000 from our existing car loan, so the blue shaded line on the table below shows that if you apply for a loan with 61-72 months, you'll pay the highest rate of 4.94% with excellent credit, but most people would most likely be well above 5%.

If you manage to pull off a lower term loan of 24 to 36 months, the table above shows your APR drops significantly down to as low as 2.24%, which is almost half the interest rate of the 6 year car loan you were about to consider applying for. For decades we have warned car shoppers to avoid all car loans greater than 48 months. No matter what your interest rate is, the shorter the loan, the less actual cash you will pay in interest.

7) Allow the finance company to auto deduct monthly payments

This little known juicy secret tidbit of car financing delight is an often overlooked benefit for you. Most lenders will shave 0.5% off your APR if you allow them to deduct your monthly auto loan payment directly from your bank account.

This is important for you because it saves you a lot of money and the bank knows they will get their payment every month. So they sweeten the deal for you by giving you that extra ½ point off.

How much does this benefit you? If you allow your lender to auto deduct instead of invoicing you every month, on a $25,000 loan for 48 months at 4% APR, the finance company lowers your interest rate to 3.5%. Your total interest paid would $2,094 at the 4% rate, but only $1,827 at the 3.5% rate.

You can see how allowing the lenders to auto deduct from your bank account saves you another $267. Just keep the savings flowing from every category on our list here and you'll save a fortune. I used this strategy myself when I bought a new Lexus SUV and financed it online for 36 months a few years back. I really enjoyed the lower interest rate. Also, I never had to write a check, the lender just deducted the car payment right out of my bank account when payment was due.

8) Come up with more money down to reduce amount borrowed

It's not rocket science folks, the more money you borrow, the more interest you'll pay. Always look for ways to put down more money on your car so you don't have to borrow as much and you your monthly payments will be lower. Sell some expensive collectibles, comics, artwork or electronics. Whatever is lying around your house or in the attic or garage might have value. If you're not using it, sell it and use the cash for your down payment.

We have always warned consumers to put down at least 20% on a new car to avoid being upside down on the car loan. We advise the minimum amount to put down on a car should be 20%. If you don't have that amount to put down, then don't buy the car until you do have the 20% to put down.

9) Send in extra principle in your monthly car payment

Sending in extra principle has the effect of lowering your interest over the life of the loan.

When I bought my first car, I was a very savvy buyer looking to save money on my financing in every nook and cranny I could squeeze a few incremental dollars out of. I sent in extra principal with my car loan payments, which accelerated the payoff on my car from 42 months down to 36 months.

How do we do that? It's all in the way mortgages and car loans work. In the early months of the loan you are paying almost no principle back and each monthly payment goes almost all to interest. But lucky for you folks, you can control this formula by forcing more principle down their throat with your monthly payments, which means you are paying the loan off sooner. Since you pay it off early, they don't get to charge you all that interest anymore.

When I first bought my house, I sent in $300 to $500 extra principle each month. Then, before you know it, I knocked over 10 years off the life of my loan and saved tens of thousands of dollars.

There you have it, I bet you never thought you had so much control over the interest you will pay on your car loan. So remember, be patient and calm. If it takes a few more months, let it happen. Pay off all credit card balances if possible, finance online directly with lenders, refinance your existing car loans to lower rates, choose a shorter term auto loan and allow the lender to deduct your monthly payment directly from your bank.

This list will maximize your interest savings when you apply for any type of financing. Let us know in the comments below any tricks you have tried.

About The Author: Jeff Ostroff

A lifelong consumer advocate with over 20 years of unparalleled expertise, Jeff is the Founder, CEO and Editor-In-Chief of CarBuyingTips.com. As chief consumer advocate, he oversees a team of experts who cover all aspects of buying and selling new and used cars including leasing and financing.

For decades, Jeff has been the recognized authority on vehicle purchasing, sought out often by the media for his decades of experience and commentary, for live call-in business radio talk shows and is cited often by the press for his expertise in savvy car shopping methods and preventing consumer scams and online fraud. Jeff has been quoted in: CNN, MSNBC, Forbes, New York Times, Consumer Reports, Wall Street Journal and many more.

Jeff also has extensive experience and expertise in new car brokering and selling used cars for clients on eBay and Craigslist. Connect with Jeff via Email or on Twitter.