Negotiating Tips and Dealer Tricks

Now that you have been able to determine how much the dealer paid for the car and you've figured out your 3% - 5% fair profit offer, you are in a much better position than most new car shoppers.

In This Chapter:

1. Your Negotiating Strategy

If you know somebody that has recently purchased a car, ask them to share their paperwork so you can familiarize yourself with the buyers form. You will know how the forms work so you won't be intimidated when it's time to close the deal. The dealer's paperwork can be very confusing by design.

Negotiating Tips:

- Don't Be a Monthly Payment Buyer

- Don't Be an Impulse Buyer

- Don't Let the Negotiation Drag On Forever

- Use Dealer Cost as the Baseline for Your Negotiation

- Stick To Your Guns

- Get Something to Eat Before Shopping

- Don't Go to the Dealership By Yourself

- Don't Be Afraid to Walk Away

- Never Give a Deposit Until Everything is Finalized

a. Don't Negotiate a Car Deal Based on Monthly Payment

Doing this will open you up to the "Cash Flow Shell Game." You must negotiate the price first, then the financing. Be especially careful when a 0% APR deal is going on. Make sure to stay focused on the purchase price at all times.

b. When Car Shopping Don't Be an Impulse Buyer

If you let your impulses take over at a car dealership it will cost you a lot of money. You can always buy tomorrow or a week from now. Take your time because good things come to those who wait!

c. Wrap Up the Negotiation with the Salesman Quickly

Try to complete the negotiation in a half hour. Much longer than that and it isn't worth the salesperson's time to give you the best deal since they will end up with as little as $50 commission. Set your "deal timer" for 30 minutes. Tell them if the deal isn't agreed upon when it goes off you will leave.

d. Negotiate Up From Dealer Cost and Not Down from MSRP

Remember from the last chapter that Invoice Price is not the actual Dealer Cost. In the last chapter I showed you how to calculate the actual Dealer Cost and formulate a fair offer of 3% - 5% above it.

e. Once You Make Your Offer, Stay Strong

Get Real Pricing on Actual Cars

Use the research in "The Folder" to justify your offer and stick to it (if you offered a 3% profit you can come up to 5%). They'll shout at you, call you names and accuse you of stealing from their kids. This is part of the dealer's game so don't agree to "split the difference." You should never end up more than a few hundred dollars over your fair offer.

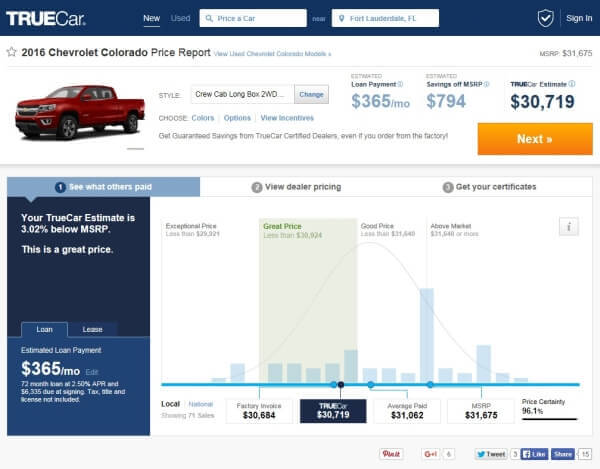

TrueCar should be your first stop on the road to backing up your offer. Use the data on the TrueCar Curve to defend your your offer against any attacks by the sales people. You will be able to see what others in your area have paid for the same car. You can also get a Guaranteed Savings Certificate from TrueCar if desire a hassle free deal. Don't let your guard down! Make sure to pay attention to all aspects of the deal.

f. Never Negotiate a Car Deal on an Empty Stomach

Before you go to negotiate eat a good meal, make sure you are rested and dressed comfortably (but nicely). Do not go car shopping if you are sick, have a fever or a headache. You want to be on top of your game at the dealership.

g. Bring Another Person With You to the Dealership

Having a second person on your side keeps the salesperson from being able to intimidate you. Strategically your partner should be a doubting Thomas, devil's advocate, constantly pointing out negative parts of a deal, trying to "talk you out of it," saying you should go back to the other dealer.

h. CarBuyingTips.com Favorite - The Power of Walking Out

If you aren't satisfied with the way the negotiation is headed then just get up and leave. This is the power that you have and it will panic them once they see you are serious. You might be halfway to you car when they stop you with a better offer.

i. Never Give a Deposit Until the Deal is Done

Unless you have agreed to everything and are buying the car there is no reason to give any money. It does not "show that your offer is serious," all it does is let them hold your money hostage. If you are ordering from the factory then a deposit is proper once the deal is signed.

Email From a Visitor Shows My Tips Work

To: Jeff

I walked out of the first deal at signing. They called me names, told me I was crazy and no one would beat the deal. I went to another dealer who discounted $1,000 from MSRP. They disclosed everything and exactly how much they were giving me for my lease pay off. They even threw in the floor mats! I drove my new car back to the first dealership to get my deposit back. I loved it!!!

2. How to tell how long a car has been on the dealer's lot?

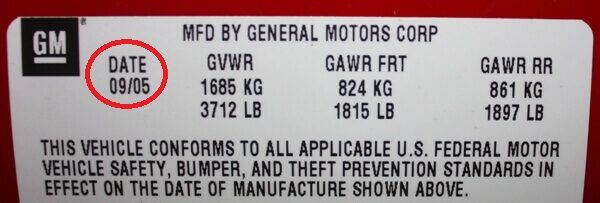

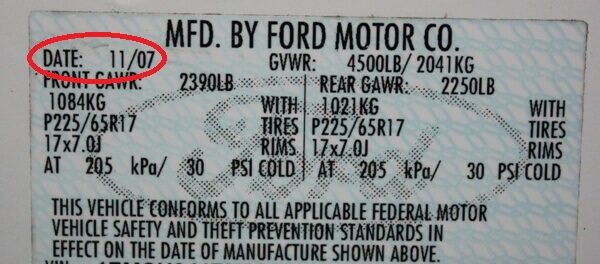

Dealers are often motivated to sell the cars that are sitting on their lot the longest. They are paying costs to carry the inventory and the longer a car is on the lot, the more it costs them. How can you tell which cars are there the longest? It is as easy as locating the manufacturers sticker that is located on the drivers door or door jamb. The date of manufacture is given in a month/year (mm/yy) format in the upper left side of the sticker. This will give you a rough idea about how long the car has been there since cars are shipped shortly after they come off the assembly line.

The date of manufacture sticker can be used in other ways as well. If the dealer has multiple identical cars on the lot and they won’t give you a better price on the oldest one, then certainly you would want to select the newest car on the lot, the one that has been sitting around shortest amount of time. If you going to pay the same amount, why wouldn’t you want the newest one?

Remember, the manufactured date only gives you a rough idea, not an exact date. It only contains the month and year. The vehicle can be manufactured any day within that month. You also need to account for shipping. This may vary greatly between manufactures (import and domestic) and where and how the vehicle was shipped (boat, rail or truck).

General Motors Manufacturers Date Sticker

Ford Manufacturers Date Sticker

3. CarBuyingTips.com Exposes Dealer Tricks

During negotiations, they'll pull every trick in the book, it's just part of negotiating. Since you are reading CarBuyingTips.com you won't fall for their tricks. Just because they write something on a piece of paper doesn't mean it is true, so don't believe everything they scribble down.

Common Dealer Tricks:

- Advertising a Price that Already Includes a Rebate

- Having Two or More Salespeople Work on Your Deal

- "No Haggle" Pricing that Isn't a Good Price

- Salesperson Listens to You When You Are Alone

- Using the Sales Tally Board to Pressure You Subconciously

a. The Hidden Rebate Tactic

I see this tactic at dealers and in newspaper ads. They list a price that is less than MSRP, making you think it is a good deal. Unfortunately the "prices include the rebate." Any rebates should be subtracted after you negotiate the price. Do not let them include the rebate in their "asking price."

b. The "Turnover" (Also Called the "TO") Scam

They keep switching salespeople to work on you and wear you down. It's harassment and it's just a waste of time. They have no intention of working with you, they just want to tire you out. Tell the salesman that they should stop this nonsense right away. Tell them you are on to the scam are walking if they keep switching.

c. "No Haggle" Usually Means "No Bargain"

Many dealers use "No Haggle" pricing to make you think you are getting a good deal. People think these dealers will never negotiate. However, you still hold the power because you can just get up and leave. Sometimes the price at these dealerships will be good but if their "No Haggle" price is more than 5% over dealer cost, then it's not a good deal and it's time to haggle or go somewhere else.

d. Beware of the Eavesdropping Salesperson!

Don't discuss anything privately if they leave you alone in the office. They could have set the phone to intercom mode and now the salesman and his boss are listening to every word you say.

e. The Psychology of the Sales Tally Board

Dealers display the tally board or point out your salesperson's totals to condition you to buy. They want you to think that they are giving good deals because they are selling so many cars.

Avoid the Games with CarBuyingTips.com

The CarBuyingTips.com Car Buying Service lets you get a guaranteed price quote without leaving your house. This exclusive program leverages volume buying power of large companies, employers and membership groups to get you a low price on a new car.

The process is simple. First, select the model that you are interested in. Next, configure the options. Once completed and submitted, you will receive a guaranteed price certificate from up to three dealers from our extensive network. When you are ready to buy, simply print out the price certificate and take it the new car dealer that provided the quote. It's that easy! No hassles, no haggles and a guaranteed low price.

Here's some lies and half truths they will use to play games with you:

- "These cars are flying off the lot like hot cakes, we have no reason to lower our price. We can get top prices because everyone wants this car right now."

- "Jeff, this deal is only good today. Tomorrow I won't be as generous. You're stealing all my profits. When you come back tomorrow, I can't promise you'll get this excellent price. 3 other buyers are looking to buy this car."

- "You're not going to find a cheaper price anywhere else..."

- "If you don't purchase these options, I won't get paid"

- "If we don't beat the competitor's price we'll give you $500!" The problem is that you won't be able to get "proper paperwork" from another dealer.

- "Sure, we have that exact car you're looking for, come on down!" Then when you arrive the car has disappeared but they have a more expensive one.

- While you are in the office the salesman talks to another "customer" interested in the same exact car. Of course, the same is there is no other customer.

4. CarBuyingTips.com Says to Shop Around

Unless they have accepted your fair offer, shop around. Just because they wrote up a deal does not mean you have to accept it. Tell the sales droid that you want to think it over. Ask for a copy or write down as many details as you can, then go to the next dealer.

All the above scams are usually eliminated when you use the discount pricing sites we've recommended.

Recommended Car Price Quote Sites

TrueCar is an online marketplace for automobile shopping that provides transparency into prices that others paid for their vehicles. Consumers engage with TrueCar Certified Dealers. You'll be able to research the vehicle you are interested in and get accurate pricing on in-stock dealer inventory. See your potential savings before heading to the dealership. Start your stress-free search

RydeShopper searches pricing from their network of dealers to find the best price. Use their simple form to select make and model and start saving. Get quotes from the maximum number of dealers to give you the upper hand. Get a Quote

Edmunds.com gives you no-hassle and no-obligation FREE price quotes. You can view actual dealer inventory and prices in your area. Find the right car for you at lowest prices available. You can also use the Edmunds True Market Value™ pricing to get the best deal. Remember, when dealers compete, you win. They also list current factory to consumer rebates, as well as secret factory to dealer incentives. If you are aware of a secret factory to dealer incentive on your car, you can negotiate a lower price. Begin the FREE Quote Process

Cars.com gives you free, no-obligation quotes from up to 3 dealers. Select your make, model, color and options. Getting quotes from multiple dealers pressures them to give discounts. Free Quote

The CarBuyingTips.com Car Buying Service lets you get a guaranteed price quote without leaving your house. This exclusive program leverages volume buying power of large companies, employers and membership groups to get you a low price. Let’s Get Started

Autobytel has 20,000 dealers, they give you free no hassle low price quotes, list automobile prices and dealer cost. Get a Quote From Autobytel

BuySide Auto Concierge Service for California Residents will get you a great price and handle everything for you. They will deliver the car to your home. Only available in California. Save by Using BuySide Auto

BuySide Auto Concierge Service for California Residents will get you a great price and handle everything for you. They will deliver the car to your home. Only available in California. Save by Using BuySide Auto

5. Getting a Good Deal is Much More than Getting a Good Price

In order to truly get a good deal, you must pay attention to more than just the price. You need to start by using the tactics that we recommend to get the best price possible but, unfortunately, your negotiating job isn't done yet. The real scams happen in the finance and insurance (F&I) office. The dealer wants you to let your guard down but you'll be ready! Keep reading our advice so that you'll be prepared.

Go to the Next Chapter: Closing the Deal, Avoiding F&I Office Scams >

New Cars Home

New Cars Home Invoice Prices Explained

Invoice Prices Explained What to Take to Dealer

What to Take to Dealer Close the Deal

Close the Deal Top 10 Dealer Scams

Top 10 Dealer Scams Misleading Ads

Misleading Ads New Car Fee Glossary

New Car Fee Glossary